Tax Changes Canada 2024

In this article we’re diving into the Canadian tax changes for the year 2024. It's crucial to stay informed, especially with how rapidly our economic landscape is evolving.

We'll discuss updates to the RRSP and TFSA contribution limits, some big changes in the CPP contribution rates, and introduce the latest on the First Home Savings Account. Plus, we'll look at examples of personal tax in 2024 compared to 2023.

🎥Or if you would rather have Joe explain it to you, check out this video below 👇

RRSP Contribution Limit Increase

First up, one of the key savings tools for Canadians – the Registered Retirement Savings Plan, commonly known as the RRSP. For those who might be new to this, you can also read through our full guide to RRSPs here.

For 2024 the maximum RRSP contribution has jumped to $31,560.

That's an increase of about $800 from 2023’s limit of $30,780, giving you more room to save for retirement tax-efficiently.

This change is particularly beneficial for those earning higher incomes. If your income is in the upper brackets, this increased limit allows you to shelter more of it from immediate taxation, which can mean a significant advantage to your wealth creation.

It's a move that acknowledges the need for more robust retirement savings, especially considering the economic shifts we've been experiencing. For many Canadians, this increased RRSP room could mean more financial security when they retire.

TFSA Contribution Limit Increase

Shifting our focus now to another significant aspect of personal finance in Canada: the Tax-Free Savings Account, or TFSA. The TFSA is an investment tool provided by the federal government, available to Canadians who are 18 years and older.

Its primary role is to offer a flexible way for individuals to save and invest their money.

Unlike RRSPs, when you contribute to a TFSA, you don't get a tax deduction upfront. However, the investments in your TFSA grow tax-free, and when you withdraw funds, you don't pay any tax on the withdrawal. This makes TFSAs a great choice for both short-term savings goals and long-term investment strategies.

In 2024, you will be able to contribute up to $7,000 to your TFSA.

This is a step up from the previous limit of $6,500 in 2023 and $6,000 in 2022. It adds more opportunity to increase your tax-free investments and savings.

For those who were 18 years old in 2009 when the TFSA was introduced, you would then have a total maximum lifetime contribution limit of $95,000 as of 2024.

For further reading on TFSAs, you can check out our full article explaining the difference between TFSAs and RRSPs.

First Home Savings Account (FHSA)

Next up, a newer development in Canadian financial planning – the First Home Savings Account, commonly referred to as FHSA. This account has been introduced to assist individuals in saving for their first home purchase. The FHSA incorporates elements from both the RRSP and the TFSA, tailored to cater specifically to first-time homebuyers.

The fundamental purpose of the FHSA is to provide a tax-advantaged way for Canadians to save for their initial foray into home ownership.

Contributions made to an FHSA are tax-deductible, similar to an RRSP, which means these contributions can reduce your taxable income.

The investment growth within the FHSA is tax-free, akin to a TFSA. When the time comes to purchase your first home, these funds can also be withdrawn tax-free, provided they are used for this specific purpose.

For the year 2024, the FHSA has specific contribution limits. The lifetime contribution cap is set at $40,000, with an annual contribution limit of $8,000. This structure allows for a decent amount to be accumulated over time helping Canadians to gather a down payment for a home.

Eligibility for opening an FHSA is straightforward: you must be a resident of Canada, at least 18 years of age, and a first-time homebuyer.

The term 'first-time homebuyer' in this context includes those who have not lived in a home they owned during the previous five years. This extends the benefit of the FHSA to a broader group, including those who may have previously owned a home but have not been homeowners recently.

To ensure the tax-free status of withdrawals, the funds must be used for the purchase of an eligible home. This condition is crucial for the FHSA to serve its intended purpose effectively.

For further reading, please check out our full article on the First Home Savings Account.

CPP Contribution Rate Increase

Next up, some big changes to the Canada Pension Plan, or CPP.

CPP is a fundamental part of Canada's social safety net, designed to provide financial support to individuals in their retirement years. In 2024, we're seeing some notable changes to the CPP that will impact both employees and employers across the country, including the self-employed.

The first thing I want to explain regarding CPP relates to your yearly maximum pensionable earnings or YMPE.

Your YMPE is basically your limit used to calculate how much of your earnings you’ll contribute to CPP in a given year.

Your maximum pensionable earnings will increase in 2024 to $68,500 which is up from $66,600 in 2023.

In addition, there is a newly added layer of CPP called the “second additional component” or just “CPP 2.0” for short. This is part of a multi-year plan to enhance the CPP and provide greater benefits in the future. CPP 2.0 adds another layer of pensionable earnings called your YAMPE or yearly additional maximum pensionable earnings.

Here’s how CPP will work in 2024.

If you earn up to the YMPE threshold of $68,500, you’ll pay a maximum of $3,867.50 in CPP contributions as an employee.

If you earn more than $68,500, you’ll move into the YAMPE threshold.

This means you’ll pay an additional 4% on earnings between $68,500 and $73,500, for a maximum CPP contribution of $4,055.50.

For employers, the increased rate requires them to match the higher contributions for their employees, impacting payroll costs.

Self-employed individuals will feel a more pronounced effect, as they are responsible for covering both the employee and employer portions of CPP contributions.

With the 2024 rate increase, self-employed individuals can pay CPP contributions up to a maximum cost of just over $8,100!

Federal Tax Bracket Changes

A perhaps more welcome change for 2024 relates to personal income tax brackets.

First a quick review of personal tax brackets. In essence, tax brackets are ranges of income taxed at specific rates. As your income increases, only the income within each bracket's range is taxed at that bracket's rate, making the system progressive.

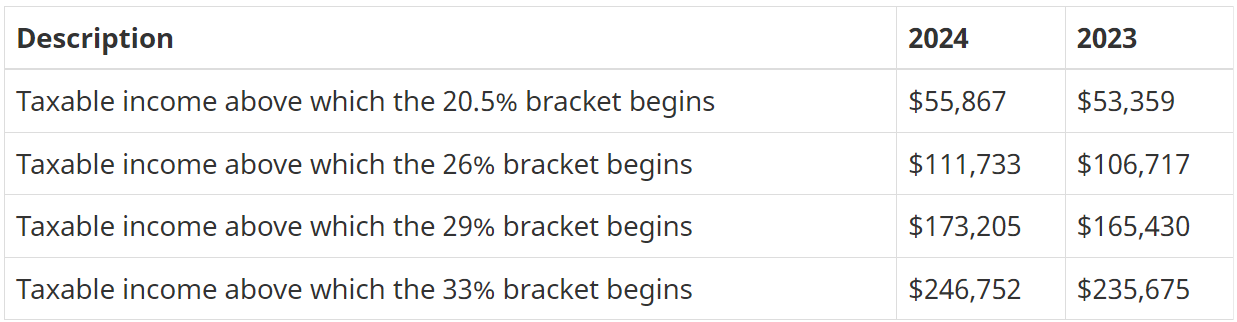

For 2024, there are adjustments to the federal tax brackets in Canada. These changes are designed to account for inflation and economic shifts.

The tax rates themselves remain unchanged; however, the income thresholds for each bracket have been increased. This means that more of your income will be taxed at lower rates compared to previous years, potentially reducing your overall tax burden.

For instance, the lowest tax bracket, which is taxed at 15%, now applies to income up to $55,867 compared to $53,359 in the previous year.

Similar adjustments have been made to subsequent brackets. These changes are beneficial as they allow Canadians to retain a larger portion of their income before moving into a higher tax bracket.

Basic Personal Amount Increase

The Basic Personal Amount, or BPA, is a non-refundable tax credit that every Canadian taxpayer can claim. It represents a portion of income that is not subject to federal income tax. The BPA ensures that individuals with low income do not pay federal income tax on a minimum amount of earnings.

In 2024, the BPA will increase to $15,705 compared to $15,000 in 2023.

The increased BPA means that a greater portion of an individual's income falls into the tax-free range, which can be particularly beneficial for those in lower income brackets. This increase in the BPA is part of ongoing adjustments to ensure the tax system reflects changes in the economy and cost of living.

2024 vs 2023 Taxes Owing

What do the tax bracket changes and basic personal amount increase mean for you?

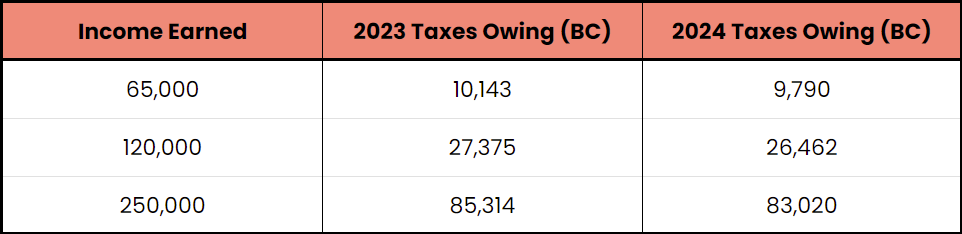

Let’s look at a few examples for a single person in BC earning employment income.

If you live in British Columbia and earn $65,000, your total taxes in 2023 would have been $10,143

Earning the same amount in 2024 means you would only pay $9,790 in tax. This shows a decrease of about $350 in taxes in 2024 compared to 2023.

For those in higher tax brackets the change is a little bit more pronounced.

BC employees earning $120,000 in 2023 would pay $27,375 in tax whereas that same income in 2024 would mean $26,462 in taxes instead which is a decrease of about $900.

And one last quick example, those earning $250,000 in BC would pay about $2,300 less in tax in 2024 compared to 2023.

So, overall we can see that total tax paid on the same amount of income decreases across the board as a result of the tax bracket and BPA changes.

Lifetime Capital Gains Exemption Increase

The Lifetime Capital Gains Exemption (LCGE) is a significant tax relief provision for Canadian business owners, particularly those who own incorporated businesses.

It enables certain Canadian entrepreneurs to sell shares of their incorporated business and not pay tax on a part of the profit they make from the sale. This means they can earn a significant amount from selling their business shares without it being taxed.

For 2024, the lifetime capital gains exemption limit has been increased to $1,016,836

This is an increase from the 2023 limit of $971,190.

For example, if I sold Avalon Accounting Inc. at a gain of just over $1 million dollars, I could potentially use my lifetime capital gains exemption and pay zero tax on that gain.

%20(8).png)

%20(7).png)