Payment Methods for Small Businesses in Canada

This article will dig into some really useful payment methods that small businesses in Canada can use. We’ll look at methods to collect payments from customers and methods to make payments to suppliers.

There are many payment options that most people know about (cash, cheque, credit card, etransfer, etc.). We’ll talk about those at the bottom of the article, but first we’ll start with some alternative methods that can really make business owners’ lives easier.

We have worked with all of the methods discussed in this article and have chosen them specifically because we think they’re the best options available right now.

Best Payment Methods for Small Businesses

We may as well cut to the chase before we dive into all of the details. Here is a list of our favorite payment methods for small businesses.

Keep scrolling after our top picks for a lot more detail and some additional payment options that can also work really well.

Best for Collecting Payments via Credit Card - Stripe

Stripe is our top payment provider when it comes to collecting payments via credit card. It’s no wonder that millions of businesses trust Stripe as a payment processor - it is easy to use, flexible and reliable.

- Stripe’s processing fees are competitive compared to other payment methods

- It’s very flexible as it integrates with a huge number of systems

- Being so widely used, the Stripe brand instills confidence in customers

- Stripe functions well with many different point of sale and accounting systems

You can’t really go wrong choosing Stripe as your payment processor for credit cards.

Best Point of Sale System - Square

If you want a point of sale system / payment processor combination, look no further than Square. Square is as simple and easy to set up as it is for customers to use. Whether you’re selling homemade goods at a market or you have multiple retail store locations, Square has a point of sale solution that will work for you.

- Square’s processing fees are competitive compared to other payment methods

- With a variety of point of sale systems, you’ll find something that fits your business perfectly

- The point of sale system user experience for both the business and customer is as good as it gets. Your accountant will be happy with the reporting capabilities too!

We always like it when our clients are using Square. It means they’ve got a great point of sale system that is easy to use for businesses and will make their customers happy.

Best for Credit Card Subscription Payments - Recurly

Recurly is great for collecting recurring payments via credit card. Recurly allows businesses (especially SAAS businesses) to manage recurring payments and various different subscriptions with a lot of flexibility. It provides detailed analytics to help businesses grow revenue and manage customer churn.

- Recurly can be a good option for businesses under $1m in revenue and above. Some alternatives are geared towards larger businesses only.

- Reasonably priced compared to other similar providers.

- Recurly is flexible and integrates well with many different systems.

- Strong analytics will help you retain customers and grow your business.

Check out Recurly first if you’re looking to manage subscriptions and collect recurring payments via credit card.

Best for Direct Debit Subscription Payments - Rotessa

For those wanting to collect payments from customers via direct debit, Rotessa is our top choice. Set it and forget it for subscription-based services or just add one-off amounts as needed.

- If your business is collecting more than 10 payments per month, Rotessa is very cost effective.

- It’s super easy to set up as a business owner with very minimal red tape and great customer service.

- Very low friction for customers to add their information and authorize direct debits.

We’ve been using Rotessa since we started and couldn’t be happier with it. Simple to use, inexpensive and payments are collected each month like clockwork.

Best for Collecting Ecommerce Payments - Shopify

Shopify is our top choice for setting up an ecommerce business and collecting payments online. Set up a beautiful store and sell your products online without any design or coding experience. The user experience is second to none which reduces friction for your customers when making purchases.

- Shopify is easy to set up. You can have a beautiful online store in a matter of a few hours without any web design or coding experience.

- One of the best shopper experiences makes it easy for people to buy from you.

- Flexible themes with many features allow you to customize your online store.

- Administration is a breeze with their simple to use back-end. Your accountant will love it too!

We always recommend checking out Shopify for existing ecommerce businesses or if you’re just getting started with an online store.

Best for Paying Vendors Electronically - Plooto

Plooto is an excellent tool for making payments to vendors electronically. Plooto is cost effective, quick and easy to use. It integrates with your accounting system to create a seamless payment process from draft to approval and payment completion.

- Straightforward pricing that is inexpensive and well worth it.

- Electronically pay vendors in Canada or internationally quickly and easily

- Reduce the administrative work required to make payments. Business owners can easily approve payments drafted by a bookkeeper and track payments in real time.

- Payments are automatically reconciled within your accounting system

We’ve been using Plooto with our clients and internally since the beginning and we love it. Definitely worth taking a look at Plooto first for your vendor payment system.

Best for Large Payment Amounts - MazumaGo

MazumaGo is the best choice for sending or receiving large payments within Canada. The platform is incredibly easy to use, there are no transaction value limits, and the pricing structure is as simple as it gets.

- No transaction value limits means you can send or receive large sums of money within Canada.

- Simple online platform uses email to send funds. Eliminate user error by never entering routing numbers or account numbers again.

- Request payment by creating a unique link and sending it to your customer in an email or an invoice.

- Straightforward pricing of 0.1% per transaction means payments are inexpensive and you’ll always know the total cost.

MazumaGo is our top choice for any business that needs to send or receive large transactions. It is also an excellent choice for sending and receiving recurring payments within Canada.

Best for Sending Money Internationally - Wise

Wise (formerly TransferWise) is our go to solution for sending payments internationally. There are no hidden fees and the exchange rates are among the best that you’ll find.

- Wise is typically the cheapest way to send money internationally. Low fees and no hidden exchange rate premiums.

- It’s easy to set up and the interface is simple to use

- Lower your foreign exchange costs by using Wise to convert your money

Wise gets it right by making it inexpensive and simple to send money internationally. We recommend checking out Wise first for exchanging your money and for sending and receiving money internationally.

Sign up for Wise through our Wise referral link and your first transfer of up to $800 will be fee-free.

How to Collect Payment from Customers via Credit Card

Collecting payments from clients and customers is one of the most important things your business needs to do.

These are some of our favorite payment methods for allowing customers to pay via credit cards.

- Stripe

- Square

- Shopify

- PayPal

Stripe

Stripe is a complete payment solution for small businesses. It integrates with e-commerce platforms and various other applications to collect credit card payments from your customers.

What Types of Businesses Use Stripe?

Stripe is a versatile yet simple solution for many businesses, including:

- Online / E-commerce businesses

- Bricks and mortar retailers

- Subscription based businesses

- Software platforms

How is Stripe Used?

We typically see Stripe integrated with other systems to collect payment. Some examples of this include:

- Integrate with Invoicing Systems - Invoice customers using accounting software like Xero or QuickBooks Online. Stripe then provides the credit card entry form for your customers to fill out and submit payment.

- Collect Payments from Your Online Store - Stripe can integrate with e-commerce platforms so that your customers can pay via credit card after adding products to a shopping cart.

- Integrate with a Point of Sale System - Stripe can integrate with a point of sale system such as LightSpeed so that you can collect credit card payments. This can be used both online and with bricks and mortar businesses.

- Custom Payment Solutions - Stripe has a versatile API that can be connected to other platforms to collect payment via credit card. Online content creators or membership-based websites are common examples.

- Paid Meetings - You can integrate Stripe with various scheduling systems like Calendly to create paid meetings. This can be used as a paywall so that payment is made before a meeting is scheduled. It’s pretty slick!

How Much Does Stripe Cost to Use? (Stripe Transaction Fees)

There is no monthly or annual subscription fee to use Stripe. The Stripe platform will withhold transaction fees each time a customer makes a purchase.

The fees for using Stripe are competitive with most similar payment collection methods.

You will pay 2.9% + $0.30 per transaction. For example:

- Customer buys a $10 item, you pay $0.59 in transaction fees ($10 * 2.9% + $0.30)

- Customer buys a $100 item, you pay $3.20 in transaction fees ($100 * 2.9% + $0.30)

- Customer buys a $1,000 item, you pay $29.30 in transaction fees ($1,000 * 2.9% + $0.30)

The Stripe website notes that volume discounts are available, but this may require significant transaction volumes before any discounts are available.

Summary

Stripe is a versatile solution that allows you to easily collect payments from your customers. It’s quick to set up and allows for a lot of different use cases.

One thing to note about Stripe is that it isn’t itself a point of sales system. It integrates with point of sales systems like LightSpeed to collect payments.

Square

Square is another excellent system for accepting credit card payments. It differs from Stripe in that Square is also a point of sale system and not just a payment processing system.

The point of sale system allows you to collect payments at physical store locations as well online and is extremely user friendly.

What Types of Businesses use Square?

- Retail

- E-commerce

- Selling goods at markets / mobile vendors

How is Square Used?

Square provides an entire range of business payment services to suit the small to medium sized enterprise market. Unlike Stripe, Square provides its own POS systems, ranging from:

- App based - download the app to your iPhone or Android device to collect payment through the Cashapp app (although this is mostly used for casual users, not businesses).

- Plug-ins to your device - card reader units connect to your phone or tablet through the headphone jack or lightning connection and can be used to swipe credit cards.

- Contactless and insert card readers - similar to credit card readers, Square’s credit card readers connect via bluetooth to your phone or tablet.

- Retail terminal systems - Square’s sleek tablet-style terminals include the software needed to sell goods for retail businesses.

- Online payments system - Square’s online payment platform is similar to other online operators like PayPal and Stripe and offers secure processing and dispute management.

Square offers a number of back-end business management services as add-ons depending on your needs and subscription.

- Inventory management - as standard with the retail terminals, the software provides all you need to manage your stock and inventory levels.

- Table reservation and scheduling software - Square’s terminals can be integrated to booking websites for restaurants, and even kitchen display units for meal orders.

How Much Does Square Cost to Use? (Square Pricing)

Square’s POS systems start at different price points (depending on your business’ scale) and a fee per transaction is charged at different rates as noted below.

For instore hardware and software, there are multiple options:

- Free app - the mobile payment app is free to download (and all software for the systems below is provided free with the card readers and terminal units)

- Free Magstripe - (1st unit free, additional units $10) - inserts to your device through the 3.5mm jack or Lightning port

- $59 for Square Reader - contactless and chip card terminal

- $199 for iPad holder & chip reader terminal - "classic countertop point of sale solution" (iPad not included)

- $399 for Square Terminal - contactless and insert card (same as a standard credit card reader). Or pay $34/month for 12 months interest free

- $899 Square Register (or 12 interest free payment of $75/month) - dual screen (customer facing and sales-staff facing)

Transaction charges vary between 2.65% and 3.4%, depending on whether it’s in-store versus online and the credit card type and entry method.

In-store

- 2.65% per tap using contactless credit or debit cards

- 3.4% + $0.15 for manually keyed-in and card-on-file payments

- $0.10 flat fee per Interac tap

Online (and Card-not-present payments)

- 2.9% + $0.30 per e-commerce transaction

- 3.4% + $0.15 per virtual terminal transaction, card-not-present or card-on-file transactions

Square also offers business invoicing through the use of its free Square Invoicing app. There are two options, free and premium, both charging based on the invoice value (between 2.65% and 3.4% depending on the card issuer and the subscription type).

The system allows for Mac, PC and mobile access for billing, emails and reporting tools. With a few clicks, any new or small business can have a professional and sophisticated system for invoicing customers.

Summary

Square is an ideal solution for the small and medium sized bricks and mortar retailer. It’s great for coffee shops, outdoor markets, and anywhere that a small portable system can be used to collect payments from customers. It’s free and quick to set up.

Its range of integrated products and services (payments, inventory management and invoicing) mean that it can more than keep up with your needs as your company grows over time.

I’m always happy to see when clients are using Square; I rarely see complaints with it.

Shopify

When Shopify was first launched, its sole product was a website builder for online retailers. Since then it has expanded into bricks and mortar store products, to compete with providers such as Square. It has in-store hardware and systems, but its key feature is still the versatile e-commerce platform.

What Types of Businesses Use Shopify?

Shopify is most suited to online retailers or physical retailers that want a strong online store, but don’t want to invest in a dedicated website.

Shopify is a webapp that is used through your browser (such as Chrome, Safari or Edge). You can simply log in to your Shopify account, select a store theme, and within minutes you can start adding items and services for your store to offer online.

How Is Shopify Used?

The platform aims to let beginners quickly and easily get set up and start an online store. There is no software to download, no coding, databases, or any other technical jargon to be understood! The system uses intuitive drag-and-drop interfaces to select the designs and layouts that you want your customers to see.

Shopify is a “hosted” website option. This means that you pay a monthly subscription and they take care of all of the maintenance of running a website (such as domain registration, servers, and hosting).

Shopify also offers their own custom hardware for collecting in-store payments (from hand-held to installed terminals) which form a fully integrated system. There are some basic reporting and analysis tools which seamlessly combine your online and in-store revenue and sales data.

How Much Does Shopify Cost? (Shopify Pricing)

There are no startup fees with Shopify. The store owner is charged a monthly subscription and a percent of each transaction through the payment system.

There are a number of subscription options:

- $29 per month - Basic: online store, 2 staff accounts and use of the card readers if purchased separately

- $79 per month - Shopify: all the Basic features, but with 5 staff accounts and some enhanced reporting features

- $299 per month - Advanced, all the Shopify features, but 15 staff accounts and more advanced reporting, customer service and currency features

- $89 per month per store location - Shopify POS Pro: offers faster workflows, greater staff permissions and advanced inventory tools for larger retail chains

You’ll get the following features with all the options above:

- An online store based on a standard Shopify template

- A payment system for collecting customer sales

- An online blog, helpful for attracting customers

- Some useful email and marketing tools

There is also a Shopify Lite option for $9/month. This is intended for integration with social media sites and would suit only the smallest of businesses (for example: Etsy users or “buy me a coffee” buttons and virtual tip jars).

Costs per transaction:

- Online Canadian Credit Cards - $0.30 per transaction plus 2.4 to 2.9% of transaction value (depending on subscription

- International/Amex Credit Cards - $0.30 per transaction plus 3.3 to 3.5%

- In-person Credit/Debit Cards - 2.4 to 2.7%

- In-person Interac - $0.10

POS hardware starts from $69 for card readers and can get into the $800 range for installed full-featured sales terminals.

Summary

Shopify is our recommended solution for e-commerce businesses that want an turn-key solution to sell goods and services online. It’s fast to set up and business owners need no coding or design skills to create a beautiful online store.

Business owners can seamlessly add bricks and mortar options with Shopify’s point of sale systems and the reporting is excellent for those (like me) who love digging into the sales data.

Shopify is another system that I’m always happy to see when we take on new clients. It’s flexible and easy to use.

PayPal

PayPal is one of the original and most popular online payment systems in the world. Most people are familiar with it as a customer for purchasing products online, but it can be a good way to collect payment for businesses.

Although PayPal offers some in-store or in person services, the majority of users only use the online elements of its service. PayPal also offers one of the best payment protection services for both customers and business of any service out there.

PayPal allows businesses to take payments in the following ways:

- In-store using QR codes and the PayPal app

- Online on dedicated business websites

- Online using marketplace websites

- Transfer funds from individuals for payments

- Collect donations online and in person at discounted rates versus business transactions

What Type of Businesses Use PayPal?

- Typically small businesses and start-ups

- Online retailers, e-commerce sites

- Increasingly used by small and medium bricks-and-mortar businesses

- Non-profits, charities and clubs

How Does PayPal Work?

Although PayPal offers some in-store or in person services, the majority of people will use the online elements of its service. PayPal also offers one of the best payment protection services for both customers and businesses of any provider out there.

PayPal for Templated Ecommerce Platforms

PayPal is highly integrated to many of the most common websites and can be as simple to activate as flipping a switch. Shopify, WooCommerce, Prestashop, Mageneto readily offer businesses the option of accepting payments through PayPal.

PayPal for Custom Ecommerce Websites

For custom websites, adding the PayPal Checkout is a quick and easy way to collect payment online. Customers are taken to a separate payment portal and can choose their preferred payment method (credit card, debit card, or pay through PayPal itself).

PayPal for In-Store Sales

PayPal can generate a QR code which you display in-store (or present to the customer in the office). This can be scanned by your customer’s phone and takes them through to a custom portal where they can make payments directly to your business. The customer must have the PayPal app downloaded to make payments and values must be entered manually.

How Much Does PayPal Cost? (PayPal Pricing)

PayPal charges for each transaction processed through the system.

- 2.9% + $0.30 fee - charged on each online transaction

- 1.9% + $0.30 fee - QR code scans for $10 an above (increases to 2.4% below $10)

- 0.8% to 1.0% fee - additional fees for foreign currency transactions

Summary

PayPal is one of the biggest online companies and the largest online payment services. It offers great flexibility to companies in terms of how to collect payments from customers (online, in-store, in-app or traditional credit card) and offers a standard fee per transaction.

There are some cheaper alternative options out there, but PayPal is amongst the most trusted online payment methods around.

How to Collect Payment from Customers by Direct Debit

For recurring and subscription services, Direct Debit is the preferred payment type for most businesses. It’s much cheaper for the business owner than accepting credit card payments.

Direct Debits (also known as Pre-Authorized Debits or PADs) allow customers to avoid having to log in to their online banking and make repeated payments to your business every month (or other billing frequency).

They eliminate the risk of a customer forgetting to pay and it greatly increases the chances of retaining a customer for multiple periods.

Below are some of the best solutions available right now.

Rotessa

Rotessa is a website and payment system which allows businesses to easily charge payments to customer’s bank accounts. I’ve listed it first because it’s our favorite option and the one we use at Avalon.

The website sends an email to your customers and provides a portal for the customer to securely add their banking details online to give approval to debit funds on a recurring basis.

The system integrates well with QuickBooks, Xero and also Zapier to access your accounting data and to automate many aspects of the payment and invoicing process.

What Types of Businesses Use Rotessa?

Rotessa is a flexible service which can be used by many business types and sizes. It is most useful for businesses with monthly recurring or subscriptions services.

- Accountants - it’s especially important to pay your accountant on time 😁

- Gyms and fitness centers

- Childcare and daycare centers

- Rent collection and property management fees

How Does Rotessa Work?

You’ll be collecting payments in just a few clicks:

- Sign Up - sign up for Rotessa for free

- Add Customers - add your customer names manually or by importing a CSV list

- Get Authorization - send your customer an authorization request by email with one click

- Schedule Payments - once your customer has completed the authorization form and entered their bank details you can add payment amounts and dates

- Cash is Deposited - you will receive your payments typically in just a few business days

How Much Does Rotessa Cost? (Rotessa Pricing)

The costs are based on the number of transactions that are processed.

There are no set up costs and no cancellation fees or minimum spend.

- $16 per month - 1 to 10 transactions per month

- $36 per month - 11 to 50 transactions per month

- $59 per month - 51 to 100 transactions per month

- $85 per month - 101 to 250 transactions per month

- $0.35 per transaction - 251 to 1000 transactions per month

- Custom pricing - custom pricing is available if you have more than 1,000 monthly transactions

- NSF Fees of $29 - for each stopped payment or NSF (Non-Sufficient Funds)

For businesses with a low number of transactions per month, it may not make sense to use Rotessa. However it’s such an easy platform to use, I would recommend giving it a try if you expect to grow to more than just a handful of monthly transactions.

Summary

Rotessa is an excellent way for small businesses to collect recurring payments from customers. Rotessa’s system is very easy to use for both businesses and customers, and it provides a professional interface.

Multiple price points means that Rotessa covers business from 1 to 1,000 recurring customers at very competitive prices.

We have used Rotessa at Avalon since 2015 and couldn’t be happier.

Plooto

Plooto describes itself as “mission control for your accounts payable and receivable”. It is a great option for a small business payment system that integrates with your existing accounting software to manage payments.

Plooto is an online web application used to make vendor payments, collect customer payments and even use for invoicing.

What Types of Businesses Use Plooto?

- Small service-based businesses

- Freelancers, contractors and sole proprietors

- Small companies with recurring payments and subscription services

- Businesses with virtual accounting departments (aka Avalon’s customers)

How to Collect Payments with Plooto

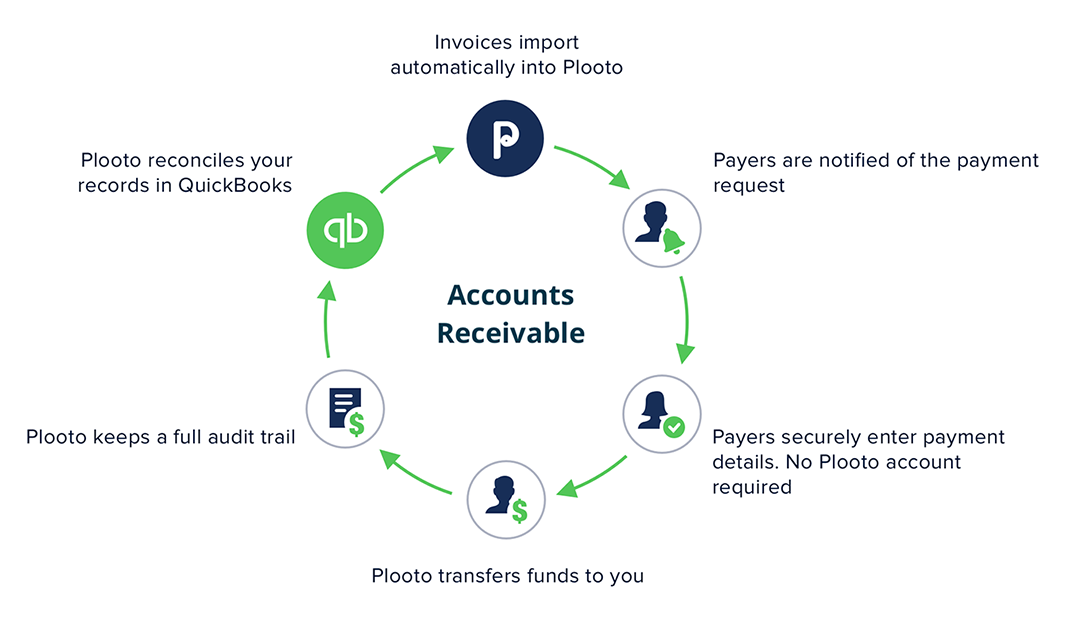

Plooto can be integrated with Xero or QuickBooks to automatically notify customers of payment requests once an invoice is created.

The process looks like this:

- Plooto is integrated with your accounting system (Xero or QuickBooks)

- All open invoices and customers are pulled in to Plooto and can be viewed on one page

- Simply click the “Request Payment from Customer” button

- Customers will receive an email with the payment amount and terms

- The customer enters details to a secure portal. No Plooto log-in or account is needed for customers

- Plooto then transfers the funds and keeps a full audit trail

- The payment is then automatically reconciled (marked as paid) within Xero or QuickBooks

Plooto has recently added the option to collect payment via credit cards as well. It works in the same way as noted above, with the customer offered credit card as a payment option in the secure portal.

How Much Does Plooto Cost to Receive Payments? (Plooto Pricing)

Plooto charges customers a subscription fee and a charge per transaction shown in the list below. Plooto’s prices are charged in USD.

- $25 per month - Monthly subscription cost

- 2.9% + $0.30 - per transaction for credit card payments

The subscription costs include

- Unlimited users per business

- Unlimited customers and suppliers

- Integration with QuickBooks and Xero

- Live support from Plooto

There is a free 30-day trial with 10 free transactions included. Plooto also offers a range of business payment transfers, cash flow analysis and reporting tools for managing your accounts.

Summary

Plooto is a great solution for small businesses to integrate their accounting systems with an easy to use payments system. It handles payment notifications, payment portals, invoicing and reconciliation in your accounting software.

We highly recommend giving Plooto a try for your business.

GoCardless

GoCardless is an online payments system that is designed to complement businesses that use direct debit as a payment method. It helps businesses to collect one-off payments from customers.

For companies which primarily use direct debit, receiving one-off payment can be difficult and expensive.

- Direct debits are not always optimized for single payments

- Credit card charges can be relatively expensive

- Bank transfers offer a poor customer experience and can be slow

GoCardless targets this part of the market by improving the process for collecting one-off payments.

What Types of Businesses Use GoCardless?

- Small service-based businesses

- Freelancers, contractors and sole proprietors

- Small companies with a mixture of recurring payments and one-off charges

How Does GoCardless Work?

- A GoCardless button or link can be added to your website, or a link can be sent directly to customers through email.

- Go Cardless connects the customer to their own bank and the customer submits the payment.

- Once the payment is made GoCardless transfers the funds to the seller’s bank account and confirmation emails are sent to all parties.

- The system is designed to be very smooth and friction-free for both the customer and business.

GoCardless also offers recurring payment and invoice management facilities as it expands its portfolio of services. It offers a wide range of integration capabilities, including Xero, Quickbooks, Zoho, Teamup, Zuora and Chargebee.

How Much Does GoCardless Cost? (GoCardless Pricing)

For domestic transactions, GoCardless charges 1% + $0.40 per transaction ($4 maximum per transaction) and an additional fee of 0.3% on values above $3,000.

Fee example:

- Payment value: $5,000

- Transaction fee: 1% * $5,000 + $0.40 = $5.40 but is capped at $4.00

- Add the High Value transaction fee: ($5,000 - $3,000) x 0.3% = $6.00

- Total charge: $10.00

For International transactions, GoCardless charges 2% + $0.40 per transaction.

There are also three subscription levels offering basic to advanced services.

- Free (Standard): free monthly subscription, pay per transaction only

- $75 per month (Plus): adds some extra customization to payment statements

- $350 per month (Pro): invite customers to set up account with your business online or over the phone, additional features and custom designed payment pages

Custom pricing options are also available for larger corporations based on a per-transaction basis.

Summary

GoCardless is a good choice for businesses that are set up to receive recurring payments or subscriptions and are not optimized for one-off payments. GoCardless makes it easy to set up both types of payments in a way that gives a smooth customer experience.

How to Collect Recurring Payments from Customers

Rotessa

Rotessa was covered in an earlier section, and we’re listing it again because it is our favorite system for managing recurring payments from customers.

There is one caveat here which is that Rotessa is used for pre-authorized debit (bank to bank) payments and not for accepting credit card payments.

Keep scrolling if you want our top choices for accepting recurring credit card payments.

What Types of Businesses Use Rotessa?

Rotessa is a flexible service which can be used by many business types and sizes. It is most useful for businesses with monthly recurring or subscriptions services. We use it for exactly that!

- Accountants and other service providers with recurring services

- Gyms and fitness centers

- Childcare and daycare centers

- Rent collection and property management fees

How Does Rotessa Work for Recurring Payments?

Recurring payments is where Rotessa really shines. Rotessa gives you the flexibility to collect payments directly from your customers’ bank accounts.

It’s easy to set up and very cost efficient:

- Sign up for Rotessa for free

- Login to the web application and navigate to the “Customers” tab

- Click “New” and enter the customer’s name and general details

- Send your customer an authorization request by email with one click

- Schedule your payments for any frequency and for any period of time, including indefinitely

It’s super slick and offers a great setup experience for both you and your customer.

How Much Does Rotessa Cost for Recurring Payments? (Rotessa Pricing)

The costs are based on the number of transactions that are processed.

There are no set up costs and no cancellation fees or minimum spend.

- $16 per month - 1 to 10 transactions per month

- $36 per month - 11 to 50 transactions per month

- $59 per month - 51 to 100 transactions per month

- $85 per month - 101 to 250 transactions per month

- $0.35 per transaction - 251 to 1000 transactions per month

- Custom pricing - custom pricing is available if you have more than 1,000 monthly transactions

- NSF Fees of $29 - for each stopped payment or NSF (Non-Sufficient Funds)

Summary

Rotessa is an excellent way for small businesses to collect recurring payments from customers. Rotessa’s system is very easy to use for both businesses and customers, and it provides a professional interface.

Multiple price points means that Rotessa covers business from 1 to 1,000 recurring customers at very competitive prices.

We have used Rotessa at Avalon since 2015 and couldn’t be happier.

Recurly

Recurly is another excellent option for payment collection if you operate a subscription-based business.

Recurly is a subscription management service and not a payment gateway. However, it offers a significant range of tools and analytics to keep your churn low and your revenue moving in the right direction.

What Types of Businesses Use Recurly?

- SaaS businesses

- Streaming and other media companies

- Popular with healthcare and education subscriptions

Recurly can handle businesses with annual revenue from under $1m to greater than $25M.

How does Recurly work?

Recurly likes to frame their tools as having 7 elements; each a part of the customer cycle.

- Subscription plan management

- Recurring billing

- Recurring payments

- Intelligent Retention

- Analytics

- Partners & Integrations

- The Recurly Platform

Recurly collects all of a customer’s current and previous subscriptions, payments, renewals data in one place. By analyzing each customer in detail, and your entire customer-base together, you can see trends, such as:

- Which locations are generating the most revenue

- Are there patterns or cycles in renewals or cancellations

- How products or feature changes impact subscriptions

Recurly makes automated invoicing and reconciliation easy by integrating with your payments gateway and your accounting software to give you a command center for your financial data.

How Much Does Recurly Cost? (Recurly Pricing)

There are 3 levels of pricing for Recurly. The prices below are for monthly billing; and there is an approximate 20% discount for annual billing versus monthly.

- Core - $199USD per month (if billed annually), plus 0.9% on revenue over $500k annually. Suggested for businesses with less than $1m annual subscription revenue.

- Professional - Price not listed (please contact recurly for cost) but suggested for businesses between $1m and $25m in annual revenue.

- Elite Services - Price not listed (please contact recurly for cost) but suggested for businesses with greater than $25m in annual revenue.

Summary

With all of the most common features and tools, but at a fraction of the costs of some of its competitors, Recurly is a cost-effective way to get superb subscription management services.

We recommend Recurly for businesses that specialize in subscription revenue and want to give customers the convenience of paying via credit card.

Chargify

Chargify is a subscription management service which goes beyond just sign-up and payment collection. Chargify intends to optimize the entire customer lifecycle including:

- Sign up

- Renewals

- Plan changes

- Personalized prices

- Promotional offers

All of these phases can be managed and optimized to improve the buyer’s experience and help retain customers.

What Types of Businesses Use Chargify?

- Subscription based businesses

- Business to business sales (B2B)

- Software as a system (Saas) solutions

- Businesses with greater than $1m in revenue

Chargify is a bit on the pricier side (starting at $599USD per month), so it may be best suited for businesses with greater than $1m in revenue.

How Does Chargify Work?

Chargify acts as a link between your website and your payments gateway, but is not a payment system itself.

It integrates with your e-commerce website and payments/accounting system to create a streamlined system for your customers with which to interact.

Chargify can deal with regular recurring subscriptions well. It also shines with more complex transaction setups like quantity-based purchasing, and metered / per unit or “stair-step” purchasing.

Chargify pulls together your data on subscription, renewals, payments and revenue to provide clear analytics on how your business is doing and where to focus. This type of information is so useful for subscription based businesses.

Through the intuitive web application, you can manage your customers' accounts and automate many of the billing and invoicing activities that take up business owners’ precious time.

To set up Chargify, you need to go through the following steps:

- Set up a website and payments system - Chargify “sits on top” of your existing website

- Set up your “product” or plan - you can add the recurring period, price, trial period, sign-up offer, set-up fees, sales tax settings and delivery settings this includes making

- Integrate with other systems: integrate Chargify with Xero, Quickbooks, Avalara, and many other common systems to make accounting easier

- Go Live - go-live with the system. Customers can access the custom pages and sign-up or subscribe to your services

- Analyze - review analytics to assess revenue, customer retention, churn and other metrics for your business

How Much Does Chargify Cost? (Chargify Pricing)

There are three subscription prices and some custom options

- Essential - $599 USD per month, plus 1% on revenue over $75k

- Standard - $1,499 USD per month, plus 0.75% over agreed revenue values

- Specialized - $3,499 USD per month, plus 0.5% over agreed revenue values

Customized options are available on request. Contect Chargify for more details.

Summary

Chargify is at the higher end of the monthly subscription costs of all of the systems that we have looked at. But it includes a comprehensive suite of tools to allow your business to gain and retain subscription customers.

How to Pay Vendors and Suppliers Electronically

Plooto

Plooto was featured earlier in our list of systems for direct debit payments. Plooto also offers a great workflow for vendor payments including a slick approval system. Plooto is our top pick for making electronic vendor payments.

Plooto integrates with Xero or QuickBooks for seamless bill payments and reconciliation in your accounting system. It’s great for businesses with virtual accounting departments.

What Types of Businesses Use Plooto?

- Online services and e-commerce businesses

- Small businesses that want to streamline their vendor payments

- Businesses with virtual accounting departments

How Does Plooto Work to Make Payments?

Plooto integrates with your accounting system to import bills that need to be paid. You can then approve and pay them in one click. Alternatively, a bookkeeper can create and send a list of vendor payments to the business owner to be approved and paid in one click.

Payments can take 3-5 business days to be completed, or you can store funds within Plooto itself and use “Plooto Instant” to pay vendors in 1-2 business days.

The process works really well, follows an intuitive path on the system, and really simplifies reconciliation of payments with your accounting software. If you have Plooto connected to your accounting system (and you should), it reconciles the bill as paid as soon as it’s approved.

How Much Does Plooto Cost to Make Vendor Payments? (Plooto Pricing)

Plooto charges a subscription for using the service and then a charge per transaction. The costs for payments are below.

- $25 per month - Monthly subscription cost (includes 10 free transactions)

- $0.50 - per transaction (after an initial 10 free transactions per month)

- 2.8% + $0.30 - per transaction for credit card payments

- $9.99 - per international transaction (including to and from the US)

- $1.99 - per cheque payment

- $3.00 - per CRA payment in Canada

Summary

Plooto’s offers a fantastic vendor payments service. The process is easy to set-up, easy to add approvers and easy to sync up with your accounting system.

We love Plooto and recommend it for small businesses that make vendor payments electronically.

MazumaGo

MazumaGo is an easy-to-use electronic payment platform that allows businesses to send payments quickly and inexpensively to other businesses.

This B2B payment solution is excellent for sending large sums of money as there are no transaction limits and very reasonable fees.

Login to the online platform and send transactions by entering the recipient’s email address. No need to enter in routing numbers or bank account details.

MazumaGo partners with BMO to securely process payments between any Canadian bank or credit union. It uses bank-grade 256-bit SSL encryption to ensure transactions are sent and received securely.

What Types of Businesses Use MazumaGo?

MazumaGo can be used by all Canadian small businesses. Where it really excels, though, is in sending larger amounts of money from business to business. There are many types of businesses that use MazumaGo.

Some of the more common examples of business types include:

- Construction companies

- Law firms

- Property managers and landlords

- Real estate businesses

- Venture capital firms

How Does MazumaGo Work?

MazumaGo allows businesses to send and receive large sums of money quickly. Once you sign up for free, you can get started sending and receiving payments.

Sending a Payment

- Initiate payment - login and send a payment to your supplier’s email address

- Authorize bank - the recipient clicks a link in their email and logs in with any Canadian bank or credit union to authorize the payment directly into their account.

- Transfer money - once the recipient accepts the payment, the funds are deposited directly into their account within 2-3 business days.

- Track progress - you can view the status of your payment at any time within the MazumaGo dashboard.

Receiving a Payment

- Send request - create a unique payment link within the MazumaGo dashboard and drop the link into an email or an invoice.

- Accept request - your customer or client will click the link and pay directly from their credit card or bank account. No sign up needed on their part.

- Track progress - track the progress of the payment in real-time in the MazumaGo dashboard.

- Collect your money - approved funds are deposited directly into your account within 2-3 business days.

You can send or receive one-time payments as well as recurring payments. It’s so easy to set up and use.

How Much Does MazumaGo Cost? (MazumaGo Pricing)

The MazumaGo pricing model is inexpensive and as simple as it gets. The cost is 0.1% of the total payment value (minimum charge of $2 per payment). There are no setup costs or subscription fees.

For example:

- $1,500 payment costs $2.00 (the minimum charge of $2.00)

- $2,500 payment costs $2.50 (0.1% of the payment amount)

- $50,000 payment costs $50 (0.1% of the payment amount)

When sending money to a supplier, the fee is only ever paid by the MazumaGo account holder.

When receiving money, the fee is also paid by the MazumaGo account holder.

The only time there is a fee to the customer is when they choose to pay via credit card.

If your customer or client pays by credit card, there will be a 3.5% transaction fee charged to them. There is no extra fee for you if your customer chooses to pay via credit card.

Use the MazumaGo fee calculator here to see how much any value of payment will cost.

Summary

MazumaGo is a fantastic way for small businesses to send and receive money within Canada.

It is especially useful for sending large amounts of money due to the fact that it has no transaction limits and the pricing structure is very reasonable.

The interface is simple and the process of sending payment to an email address instead of a routing number reduces the chance of error.

We definitely recommend checking out MazumaGo for any small business that wants to electronically send or receive payments within Canada.

MazumaGo is our top choice for businesses sending and receiving larger transactions in Canada.

Veem

Veem is an excellent alternative to traditional wire transfers and banking transactions.

Veem aims to be the tool of choice for companies by offering quick transaction times, favorable exchange rates, no transaction limits and the ability to track payments in progress.

The process is quite similar to Plooto and the cost is slightly less than Plooto as well. We’ve listed it as our second choice because the interface is slightly clumsier and we tend to see more businesses sticking with Plooto.

However, Veem is a great option and allows businesses to make payments quickly through its web application and accounting system integrations.

What Types of Businesses Use Veem?

- Online services and e-commerce businesses

- Small businesses with virtual accounting departments

- Small businesses looking for free domestic electronic payments

How Does Veem Work?

Veem is a web application, so it works with all common web browsers and no software is required to be downloaded.

Veem takes just a few steps to get started making payments.

- Sign up for a free Veem account - this is really quick and easy, and only takes a few minutes

- Connect your bank account - link your bank account with your Veem account so that you can access funds

- Make your first transaction - you can make payments using names and emails, and in most cases, you don’t need bank account details to complete the transaction. It also integrates with your accounting system to import bills directly from Xero or QBO.

- Notify buyers or suppliers - Veem can be set up to notify customers or suppliers of payments for your business

- Track your money from start to finish - you can track your payments from when you hit the submit button, through processing, until it is confirmed in the payee’s bank account.

- Integrate with your accounting system - watch as the payments are reconciled against outstanding bills in your accounting system via the integration.

Payment with credit or debit cards is limited to US regions. You will need to transfer funds into your Veem account to send payments from Canada.

How Much Does Veem Cost? (Veem Pricing)

Veem charges no sign-up fees or subscription rates.

The majority of transaction types are free of charge using Veem, including the following:

- ACH/EFT (bank to bank payments) - Free

- International wire to bank account - Free

- Veem wallet transactions (an app similar to Apple Pay or Google Pay) - Free

Cross-border payments from Canada to international regions have no per transaction charge, but Veem charges an exchange rate premium. This is common practice for payment providers and Veem’s rate is generally competitive with other similar platforms.

Summary

If you run a business that sends and receives many online payments, Veem can be a highly cost effective alternative to regular banks. It’s a great platform (quite similar to Plooto) and offers free domestic payments.

Veem helps you to save time and transaction fees, and payments are fully traceable from start to finish. Take a look at both Veem and Plooto if it sounds like a good fit for your business.

PayPal

In an earlier section, we covered how you can use PayPal to collect payments from customers.

PayPal is quite versatile and is a decent option for making vendor payments as well.

What Types of Businesses Use PayPal for Payments?

- Small and medium enterprises

- Start-ups, freelancers

- Online businesses

How Does PayPal Work to Make Payments?

Payments can be made through PayPal’s online web application or via PayPal’s mobile application.

For businesses wanting to pay suppliers or large organizations, the PayPal Business Account is the most suitable method of using the service.

To make payments follow the steps below:

- Set up a PayPal Business Account - this can be set up in as little as 15 minutes

- Log in to the app. Click on the Pay/Send Money tab

- Add a new contact (if required) or select the contact from your contacts list

- Select the method of payment, you can select payment (bank account, credit card or PayPal balance)

- Send payment and the transaction is complete

How Much Does PayPal Cost for Making Payments? (PayPal Pricing)

Setting up a PayPal Business Account is free. This gives you the ability to send payments and collect payments.

PayPal charges a per transaction fee to fund payments with your credit card. The cost is 2.9% + $0.30 per transaction.

If you use your bank account or PayPal balance there is no fee to send money.

Summary

Using PayPal to make payments as a business can be convenient, especially when starting out. The fees are relatively low and setup is quick and easy.

However, making payments to suppliers and large organizations can appear to lack legitimacy versus some of the more professional or business-only payment systems. This should be considered when deciding on your long term payments system.

How to Send International Payments from Canada

Wise (Formerly TransferWise)

Wise is a payments service which focuses on international payments with very competitive exchange rates compared to traditional banks and exchange services.

Wise lets you transfer funds to over 80 countries and claims to be up to 6 times cheaper than banks and 19 times cheaper than PayPal. This is a pretty impressive claim and they have a tool to demonstrate the savings so you can see for yourself.

What Types of Businesses Use Wise?

- Businesses that regularly send or receive international payments

- Freelancers, online businesses and e-commerce

- Pretty much any small business that wants to save on international transaction costs

How Does Wise work?

Wise values transparency. To this end, before you sign up for an account or send a payment, you can check the exact rate that you will be charged for your transaction. The steps to setting up an account and making a transfer are:

- Sign up for a free account - this only takes a few minutes and is easy to complete

- Set up your transfer - add the details of your payee, the value and the currencies

- Pay for the transfer - send your money with a bank transfer, debit card or credit card

- The payment is processed - the majority of payments are completed immediately, some are within a few hours, and depending on your currency and bank details they can can take up to 2 days

How much does Wise cost? (Wise Pricing)

Wise accounts are free and there are no monthly or annual subscription fees.

The way Wise makes money is by charging a premium on the exchange rates when you transfer internationally. This is the same as all other banks and payments systems, but Wise offers extremely competitive rates to customers.

So overall, this is a highly cost effective way of transferring funds across borders.

As exchange rates fluctuate so much, it’s hard to show the exact cost of using Wise and the savings versus other payment methods.

An example at today’s exchange rates for the Canadian dollar to USD is shown below, with some relevant comparison costs for other banks and systems.

In this quick comparison, some key points are:

- Wise will show you the cheapest way to transfer your funds, even if that is with another provider.

- The payee receives over $25 more using Wise than PayPal. Even though PayPal’s transaction rate is lower, its exchange rate makes it more expensive.

Wise Promotion Code

Sign up for Wise through our Wise referral link and your first transfer of up to $800 will be fee-free.

Summary

Setting up a Wise account is a “wise move” - sorry! - for all small Canadian businesses. Wise is our top choice for sending and receiving international payments.

It’s free to set up and you can check the cost of any transaction before sending. It's also easy and quick to compare to other sites and banks (through Wise’s own website) so you also know you are getting the best deal.

OFX

OFX is a similar service to Wise in that they offer electronic international payments at low cost to the transferor. You can transfer funds to over 50 currencies to over 190 countries.

OFX allows you to check rates before you make payments and track your transfers online or through a mobile app.

What Types of Businesses Use OFX?

- Businesses that regularly send or receive international payments

- Freelancers, online businesses and e-commerce

- Small business looking to save on international transaction costs

How Does OFX Work?

Use the OFX web application to send or receive money in a few quick steps.

- Sign up for a free OFX account (takes about 5 minute)

- Enter your recipient details and enter the amount to send.

- Track your transfer online or via the mobile app. Most transfers are delivered within 24 hours.

It’s definitely an easy way to send money internationally and allows you to keep track of when the funds will be delivered.

How Much Does OFX Cost? (OFX Pricing)

There is no sign-up fee or monthly subscription fee. OFX makes money by charging a small transaction fee on transfers under $10k plus a premium on foreign exchange rates.

The good news is that the foreign exchange premium can be significantly less than what other institutions would charge for the same transaction.

In this example from the OFX website, you could save between $150 and $300 USD on a $20,000 CAD to USD transfer compared to the big banks.

Summary

OFX is another great option if your business sends or receives foreign currency transactions.

It is quite comparable to Wise when it comes to cost and flexibility and has a great user interface.

The reasons we’ve listed it below Wise is that it has been a less popular option with our clients than Wise and also includes a $15 transfer fee on amounts under $10k.

PayPal (International Payments Via Xoom)

We have covered PayPal already twice in our review. Such is the reach and flexibility of the online payment system, that it can provide so many different services to customers in so many different situations.

How does PayPal Work for International Payments?

PayPal can be used to pay international vendors and suppliers electronically. This can be done using the personal app or the PayPal Business Account.

How much Does PayPal Cost for International Payments?

The rate charged depends on whether you are sending to another PayPal account or to a bank account (or other similar system)..

- Pay to a PayPal account - 5% + $0.99 (capped at $4.99 per transaction)

- Pay to a Bank account - 2.9% + $0.30

To make a payment converting from or to USD or CAD, PayPal charges a rate of 3.5% of the transaction, on top of the charges above. PayPal charges 4% for all other currency conversions.

Summary

If you already have a PayPal account and just want to send an international transaction here and there, it can be a good option. If you are sending international transactions more often, we recommend checking out Wise or OFX.

Wire Transfers

Unlike some of the other options we have covered, wire transfers have been around since the 1970s. They are a more traditional method of transferring money to and from customers. The payments are sent directly from one bank account to another using account details.

Wire transfers are most commonly used when large payments must be made quickly. Many people are familiar with wire transfers from purchasing cars, placing a deposit on a house, or similar large payments.

They are an option for some small businesses to make payments to suppliers and vendors, especially when the transfers are to another country.

What Types of Businesses Use Wire Transfers:

- Businesses that deal in large and one-off payments (eg real estate)

- Businesses that deal with companies or institutions that only accept bank account payments

- Situations where payments must be made and received quickly

How do Wire Transfers work?

International wire transfers are payments made using one of the more traditional banking systems, such as Society for Worldwide Interbank Financial Telecommunication (SWIFT) or Fedwire in the US.

To complete a wire transfer, the sender will need:

- The recipient's (or payee’s) name

- Their bank account number

- Their routing number, which is the bank’s SWIFT code for international transfers

- The amount being transferred

- You must have the funds upfront (in your bank account or in cash)

- Some providers will also require the recipient’s address and contact details in some cases (for example, with non-bank providers, such as Western Union)

How much do Wire Transfers Cost?

There can be charges to send or receive a wire transfer and the cost depends on the service provider.

Most Canadian banks charge a set fee per international wire transfer, between $15-40 depending on the bank. Some banks charge up to 2% for foreign exchange services.

Summary

Wire transfers are amongst the oldest methods of transferring funds internationally. They are nearly universally accepted once the payee has a bank account.

They are, however, one of the more expensive options on our list, but are useful when large payments must be made and cleared quickly.

Traditional Payment Methods for Small Businesses

Sometimes the most effective way to make or collect payments are the tried and trusted methods such as cash, cheque, credit card and e-transfer.

These methods have been around forever, are almost universally accepted and are secure ways to ensure funds are transferred. Depending on how you choose to use them, they can be a challenge in terms of speed or cost versus some of the other methods on our list, but read on to see how to use them in the most effective way.

Credit Card

Credit cards have been in use since 1921 with the Diner’s Club card one of the first “universal payment cards”. It is estimated that there are 2.8 billion credit cards in the world and over 350 billion credit card transactions each year. The ability to accept and process credit cards therefore is vital to a huge number of businesses.

If you run a small business such as a small store, service company or food outlet, offering the ability to pay by credit card adds more legitimacy to your business, than accepting payment through cash or e-transfer only.

What Types of Businesses Use Credit Cards?

- Small, medium and large businesses/corporations accept credit cards

- Bricks and mortar as well as online businesses

- eCommerce businesses

- Pretty much any business willing to pay the transaction fees

How Do Credit Cards Work?

There are a number of way of collecting payment through credit cards

- Collecting the details in-person/in-store or over the phone

- Using a card reader

- Processing the payment online

Your company might be suited to some or all of the methods above and this depends on the type of market you are in, your target customers and the maturity of the business.

There are a number of steps to getting your store or business set up to accept credit cards. You may already have some of these steps in place if you accept any other payment method.

Choose a point of sale and payment processing service

In choosing a payment processor, consider if all major cards and systems are accepted and the rates charged by the company.

For in-store payments, Lightspeed, Touchbistro, Clover and Square are all quite common point of sale systems that accept credit cards.

For online payments, PayPal, Apple Pay, Stripe and Shopify are common options to choose from.

Set up your payment hardware/software

If your business is a bricks-and-mortar store or outlet, you will need a point-of sale-system, card readers or terminals for accepting credit card payments.

Your online payment system will also need to be set-up with integrated software to allow customers to checkout with your goods or services and make payments.

Many payment processing services provide both physical point of sale systems as well as integrated online portals for collecting payments

Set-up your online storefront

If your business is partially or wholly online then you will need to have a storefront or e-commerce website to allow customers to navigate through your products or services, and make purchases and payments.

There are many website builders out there, and sites like Shopify make it really easy to integrate your payment system to their sites

Important Considerations When Offering Credit Card Payments

Fraud

Some credit cards are safer than others, and businesses can face a large price for fraudulent payments.

Verify addresses if possible and make sure your staff are familiar with the most common signs of credit card fraud.

Businesses face the full liability of lost or stolen credit cards used in your store or online.

Chargebacks

Chargebacks are when a payment is made but then disputed by the customer. This can be caused by complaints about the service or product, delivery failure or can be some other form of grievance from the customer.

Chargebacks can take up a lot of time and focus for business owners when challenging these disputes.

How Much Do Credit Cards Cost?

The charges from collecting payment using a credit card depend on a number of factors:

- Whether the payment was in-store, on the phone or online

- Your bank, card issuer and payment processors (there are normally 3 or 4 financial institutions involved in completing a credit card payment)

- The value of the transaction and the currency

- Whether you are being charged per transaction only, or if there is also a flat fee per transaction

- The chargeback rate; this is the charge (on top of the refund value) that the issuer charges you for processing the refund

On average, for small businesses, credit cards cost between 2.5% and 4.5% of the transaction charges.

You may need to factor in monthly or quarterly fees (amounting to 1-2%) and chargeback fees of up to $50 per dispute.

You must also take into account the cost of the point-of-sales system (or terminal) which ranges from $200-$1000 depending on connectivity and portability.

The most cost effective way to collect payments using a credit card is to

- Collect in-store using a POS: this is cheaper due to the security of the method, and the issuers charge less per transaction than over the phone or online.

- Use credit card authorization forms: this is a form signed by the customer (for repeat business) which authorizes the charging of their card).

- Use a payment processor with competitive rates: as covered in earlier sections, companies like Square, Stripe and PayPal offer competitive and transparent rates. But shop around for the best rates as variable rate deals can be even more competitive at times

Summary

Offering customers the ability to make payments using credit cards can gain or retain customers due to the widespread use and speed of processing. People also love earning rewards points by using their credit cards to make purchases.

Consider ways to optimize their use and how offering payment via credit cards can complement other more cost-effective methods of receiving payments for your business.

e-Transfer

It is estimated that there were over 240 million transfers using Interac e-Transfer last year in Canada.

This figure shows that e-transfers are well known and trusted by millions of Canadian customers due to their ease of use and convenience.

Used mostly by peer-to-peer transfers and one-off payments, it can be a useful method of payment to offer to customers in certain situations.

What Types of Businesses Use e-Transfers?

- Early-stage businesses

- Part-time or side hustle businesses

- Some small to medium businesses using e-transfer for certain payments

How Do e-Transfers Work?

e-Transfer uses online banking, email and a security question to transfer funds from one account to another.

To receive e-Transfer payments, both the customer and the business must have registered online banking services with a Canadian financial institution. You also need to share your email address or phone number and some other contact details with the customer before payments can be processed.

To make a payment using e-Transfer, the customer needs to:

- Log in to their online banking

- Add your business’s name and email address or phone number

- Select Interac e-transfer

- Add the payment value

- Enter a security question

- The funds are immediately debited from the customers account

To receive the funds the business needs to:

- Open the email or text message

- Log-in to the portal from the included link

- Answer the security question

- The funds are deposited into your account almost immediately.

For businesses, there are options to remove some of the friction from the process:

- Autodeposit - registering for Autodeposit means that you don’t need to check email or answer security questions for each transfer.

- Bulk payments - if you are looking to use e-Transfers as a way of paying suppliers, e-Transfer Bulk Payables can be used. This allows you to send payments to multiple accounts using an easy and secure file-upload system

How Much Do e-Transfers Cost?

It’s free to receive and deposit Interac e-Transfers.

To send an e-Transfer usually costs between $1 and $1.50, depending on your banking institution and type of bank account.

Some banks include a number of e-transfers as part of a monthly account package.

There are sending and receiving limits using e-Transfers. These vary slightly from bank to bank but are typically:

Sending limits:

- Per day/transfer limit: $3,000

- Per week: $10,000

- Per month: $20,000

Receiving limits:

- Per day/transfer limit: $10,000

- Per week: $25,000 - $70,000

- Per month: $50,000 - $300,000

Summary

e-Transfer is more commonly used for informal payments, when other payment methods are not available, or when a business is starting out.

However, it can be a useful and convenient method to collect payment from customers in some scenarios. Consider registering your business for auto-deposit to reduce the friction receiving funds by e-transfer.

Cash

They say that cash is king. And for many small businesses, this is truly still the case.

Given the set-up time and costs, transaction charges, monthly fees and dispute resolution charges for some of the other payment methods, it’s no wonder that cash is still such a common method of payment for a lot of small businesses.

What Types of Businesses Use Cash?

- Restaurants, bars, food outlets

- Retail business, both large and small

- Any in-person services or sales

How Does Cash Work?

If you are here reading this article, it’s safe to assume you know how cash works!

Briefly, cash is legal tender in notes or coins that is exchanged for goods and services. It can generally be used for almost any in-person retail or service situation. Unlike all of the other payment methods in this article, cash requires no further “processing” after the payment is made.

The use of cash however is declining as we are relying on electronic transfers and mobile devices for making payments more and more. It is also more susceptible to loss or theft than other payment methods.

How Much Does Handling Cash Cost?

Cash is a very cost-effective method of collecting payment from customers. There are no transaction fees, processing/handling charges and no delays or clearance periods.

You might think that dealing in cash reduces your transaction fees to zero. But there are still a number of costs to consider. There are also associated time and security costs to factor in when dealing with cash.

- Registers and till - Unlike some methods in this article, handling physical cash as payment requires storage, usually in the form of a cash register or till. These can range in cost from $300 up to $1500 or higher for integrated POS and inventory management systems

- Safe, vault and instore handling - If your business handles more than a few hundred dollars, then a safe, vault or cash transfer system could be needed for security. Cash boxes and safes can cost from $500 up to $5,000 depending on the size and requirements. Cash transfers systems (such as those used in supermarkets to transfer cash from registers to cash rooms) can cost thousands of dollars and require back-room staff and other security measures

- Security staff and time for reconciliation - Depending on the value of transactions and the amount of cash handled, in-store security could be needed. Don’t forget that handling cash means you or your employees will need to count, reconcile and transfer the cash (at least) daily. There is a time and cost burden in doing this versus cashless methods.

- Cash-in-transit services - Cash and coins for most businesses need to be brought to the bank daily or several times per week (depending on the value). Many business owners do this themselves or ask a trusted staff member. Safety can be a concern, so cash-in-transit services may be appropriate to use (examples are Brinks or GardaWorld).

Most banks are free to deposit cash and coins. However, some banking institutions or types of bank accounts charge a small fee for the number of deposits per month or deposits over a certain value (for example 0.25% above $5,000).

Summary

Cash still plays a major role in the economy as a fast, reliable, almost-universally accepted payment method. But handling cash can be time consuming in terms of storage and reconciling values, and staff costs for cash rooms and security.

Cheque

With the rise of electronic payments, the popularity of cheques has been decreasing over the last couple of decades. However, it is estimated that there are approximately one billion cheques written in Canada each year.

Throughout the world, the humble cheque is enduring year after year. Despite numerous other methods available, there are still many situations where cheques are the most suitable, or only method of payment.

What Types of Businesses Use Cheques?

- Rental payments and other property related businesses

- Large retail purchases such as cars or equipment

- Old school legal or accounting offices

- In situations where cash cannot be handled and electronic methods are not possible

How Do Cheques Work?

A cheque is a written and signed instruction to a bank to pay a specified amount to the bearer (the person presenting the cheque) or a specific named person or organization.

The “drawer” of the cheque is the person who writes the cheque and is making the payment. The “bearer” is the person getting paid.

There are a number of different types of cheques:

- Open cheques: this is a cheque that can be redeemed by the person it is given to, or passed on to someone else as payment and the third individual can redeem the cheque at the bank.

- Counter-signed cheque: this is a cheque with an individual’s name written on it; and that person signs the back and passes it on to someone else.

- Crossed cheque: a crossed cheque has a named payee and then marked with two diagonal lines across the front. This means that only the named payee can redeem the cheque and it cannot be passed on to anyone else

- Bounced cheque: a cheque bounces when the payee tries to redeem the value of the cheque with a bank, but there are not enough funds in the drawer’s account.

- Certified cheque: this is a type of cheque for which the bank has certified that there are sufficient funds in the drawer’s account. The bank holds these funds until the cheque is redeemed. This protects the bearer and gives confidence that the cheque will not bounce.

- Stopped/canceled cheque: this is where the drawer of the cheque notifies their bank to cancel the payment if the cheque is presented for payment. This can be done after the cheque has been handed over to the payee, and without notification. Unless you have received a certified cheque, there is no way to tell if a cheque has been canceled until you try to redeem it

- Post-dated cheque: this is where the drawer specifies a date after which the cheque can be redeemed. The bank is instructed to hold off on cashing or lodging the cheque until after that date

- Stale cheque: a stale cheque is one that has expired due to the time that has passed since it was written and issued. A cheque is considered stale after 3 months

- Cheque made out to “cash” Cheques that are made to “cash” can be paid immediately to the bearer.

Most standard cheques take up to two days to clear, but can take longer depending on the value of the cheque or the type of bank account used.

How Much Do Cheques Cost:

Cheques are usually free for the bearer to cash or deposit. The charges are generally applied to the drawer.

You can cash or deposit a cheque in any bank or credit union (regardless of your branch). Some financial institutions charge a small fee for cashing a cheque (up to $10 per cheque).

Cheques also have costs that are incurred by the individual or organization making the payment. These include.

- Ordering a cheque book: cheques can cost between $20 and $75 (for between 20-50 cheques)

- Bank clearance charge: this is the cost of processing the cheque. This can be included in monthly bank fees or can range between $5-$15 depending on your bank account type.

If there are any issues with your cheque, the following charges could also come into effect:

- Stop payment charges: when a drawer instructs their bank to cancel payment on a cheque, the bank will charge up to $50 to the drawer.

- NSF (Non-Sufficient Funds) charges: If there are not enough funds in the account when the payee attempts to redeem the cheque, the bank will charge a processing fee of between $10-20 per cheque.

Summary

Cheques still serve a purpose in today’s economy in situations where handling cash isn’t an option. Using some of the safety features and practices listed above can avoid some of the issues around using cheques for payment.

%20(8).png)

%20(7).png)